Picture this: It’s 2:00 AM. Your phone buzzed with an emergency call from a family member, and now you’re standing in the cold, sterile lobby of a private hospital. The doctors are incredibly efficient, but the administration desk is handed a stack of forms. Your heart is racing, not just because of the medical situation, but because of a nagging, quiet dread in your stomach: Will my insurance actually cover this?

If you have ever felt that sudden spike of anxiety, let me assure you, you are far from alone. Most of us treat buying a health insurance policy like paying taxes a chore we want to get over with as quickly and cheaply as possible. We go online, sort by ‘lowest premium’, click buy, and tuck the PDF away in a forgotten email folder. But here is the cold, hard truth: a bad health insurance policy is worse than having no insurance at all, because it gives you a false sense of security until the exact moment that security evaporates.

Let’s talk honestly about how to navigate this maze. With medical inflation in India climbing at an alarming rate of 14% to 15% every single year, a single major hospitalization can instantly wipe out years of hard-earned savings. Today, we are going to break down exactly how to choose the right health insurance plan without drowning in confusing legal jargon, so you can protect both your family’s health and your wealth.

The Illusion of “Full Coverage” (And Why Your Corporate Plan Isn’t Enough)

Let’s address the elephant in the room first: your office health cover. Almost every corporate employee I talk to says, “Oh, I don’t need to buy personal health insurance. My company covers me for up to 3 or 5 Lakhs.”

I used to believe this was a solid safety net too, until I saw a close colleague get laid off during a corporate restructuring. The very next week, his father suffered a mild stroke. Because his job was gone, his corporate insurance had expired instantly. He had to pay the entire hospital bill out of his own pocket. It was a brutal realization. Corporate plans are fantastic as a secondary cushion, but relying on them as your sole shield is like renting an umbrella the moment the wind blows too hard, the owner might just take it back.

If you’ve ever looked at other safety nets, like finding thebest car insurance planfor your vehicle, you know that buying protection is all about reading the fine print. The same logic applies here, but with much higher stakes. When you buy your own independent policy, you own it. It stays with you when you switch jobs, start a business, or take a career break. It is your permanent financial anchor.

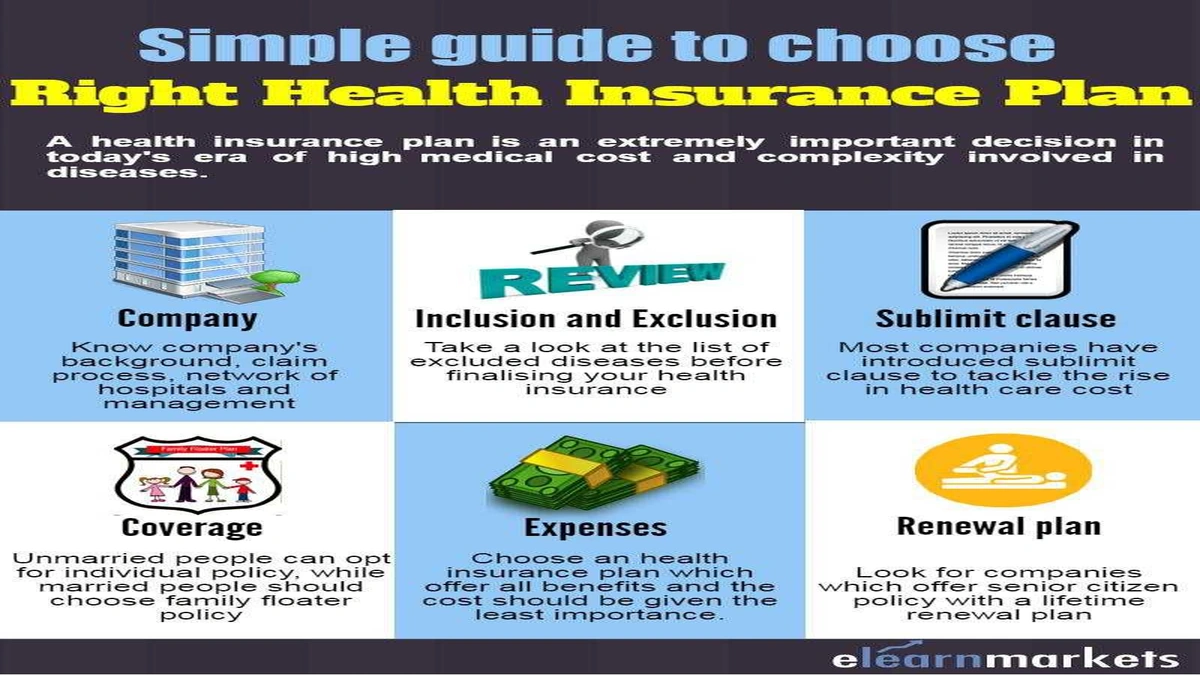

Decoding the Jargon | The Stuff They Hide in the Fine Print

Insurance companies love complex terminology. They wrap simple concepts in heavy words to make things sound more technical than they actually are. Let’s strip away the fluff and look at the real terms that will actually affect your wallet when you make a claim.

1. Room Rent Limits (The Silent Budget Killer)

This is where most people get caught off guard. Let’s say your policy has a room rent cap of 1% of your total sum insured. If your sum insured is ₹3 Lakhs, your room rent limit is ₹3,000 per day. But if you get admitted to a hospital in a metro city, a decent semi-private room can easily cost ₹6,000 per day.

Now, you might think, “That’s fine, I’ll just pay the difference of ₹3,000 per day myself.” Here’s the catch: insurers apply proportionate deduction. If your room rent exceeds your limit, they will scale down all associated costs surgeon fees, diagnostic tests, operating theater charges by that same ratio. Suddenly, a tiny ₹3,000 difference in room rent turns into a ₹50,000 deduction on your final bill settlement. To avoid this, always look for plans with No Room Rent Caps .

2. The Dreaded Co-payment Clause

A co-payment clause is an agreement where you agree to pay a certain percentage of every single claim out of your own pocket. For instance, if you have a 20% co-pay on a ₹2 Lakh hospital bill, you have to pay ₹40,000, and the insurer pays the rest. While this might lower your annual health insurance premium, it defeats the entire purpose of having complete financial protection. Unless you are buying a policy for a senior citizen where co-pay is sometimes mandatory, try your absolute best to choose a plan with a 0% co-payment clause.

3. Pre-existing Diseases Waiting Period

If you have diabetes, hypertension, or thyroid issues when you buy your policy, they are classified as pre-existing conditions. Insurers won’t cover treatments related to these illnesses on day one. They implement a pre-existing diseases waiting period, which typically ranges from 2 to 4 years. When you are assessing plans, look closely at this waiting period. If you can find a plan that offers a 2-year waiting period instead of 4, it is almost always worth paying a slightly higher premium for.

The Step-by-Step Blueprint to Select Your Shield

Now that we understand the jargon, let’s walk through the actual, practical process of choosing your plan. Think of this as your personal checklist.

Step 1 | Calculate the Real Sum Insured You Need

How much coverage is actually enough? A decade ago, a ₹3 Lakh cover was considered massive. Today, with rapid inflation, that is barely enough for a minor procedure. As a rule of thumb, if you live in a tier-1 or tier-2 city in India, your base health insurance coverage should be at least ₹10 Lakhs. If you are buying a policy for a family of three or four, aim for a minimum of ₹15 Lakhs to ₹20 Lakhs. It sounds like a lot, but the premium difference between a ₹5 Lakh policy and a ₹10 Lakh policy is surprisingly small.

Step 2 | Choose Between Individual and Family Floater

If you are young and single, an individual plan is a no-brainer. But if you have a spouse and children, a family floater policy is usually the most cost-effective route. It pools the sum insured so that any family member can use it. However, if you are looking to cover elderly parents, keep them on a separate individual policy. Mixing older parents with young families in a single floater plan spikes the premium for everyone, because the pricing is always calculated based on the age of the oldest member in the group.

Step 3 | Check the Claim Settlement Ratio and Process

Never buy a policy without checking the insurer’s track record. The claim settlement ratio (CSR) tells you the percentage of claims the company has approved out of the total claims received. Look for insurers with a CSR above 95% consistently over the last three years. TheInsurance Regulatory and Development Authority of India (IRDAI)publishes these official metrics annually, so you don’t have to rely on marketing brochures.

Equally important is checking the list of network hospitals. You want an insurer that has a wide tie-up with the best hospitals in your immediate neighborhood. In a medical crisis, you want to drive to the nearest hospital and get a cashless hospitalization without having to worry about paying cash and filing for reimbursement weeks later.

Just as you would explore ahello-worldlevel guide to understanding basic asset coverage, you need to dissect your medical security layer by layer. Take your time, compare at least three different providers, and don’t rush the process.

Add-ons That Are Actually Worth Your Money

Most insurance agents will try to upsell you a dozen different riders. You don’t need most of them, but there are two that I highly recommend considering:

- No Claim Bonus (NCB) Protector: If you don’t make a claim in a year, insurers reward you by increasing your sum insured by 10% to 50% at no extra cost. An NCB protector rider ensures that even if you make a small claim, your accumulated bonus doesn’t get wiped out completely.

- Critical Illness Cover: A standard policy covers your hospital bill. But if you are diagnosed with a major life-altering disease like cancer or a major kidney failure, the lifestyle costs, recovery expenses, and loss of income can devastate you. A critical illness cover pays out a lump sum amount upon diagnosis, which you can use for anything you need, inside or outside the hospital.

FAQs About Choosing Health Insurance

What if I forgot to declare a minor medical condition when buying the policy?

Always declare every single detail honestly, even if it is a minor issue like thyroid or an old fracture. Failing to disclose medical history is the number one reason insurers reject claims later on under the pretext of ‘non-disclosure of facts’. It is always better to pay a slightly higher premium now than to have your claim rejected when you need it most.

Can I change my health plan later if I’m unhappy with my insurer?

Yes, absolutely. Under the IRDAI portability rules, you can port your health insurance policy to another insurer without losing the benefits you have accumulated, such as your waiting period credits for pre-existing diseases. Just make sure to initiate the porting process at least 45 days before your current policy expires.

Is a cheaper health insurance premium always a bad sign?

Not always, but extremely low premiums usually come with hidden trade-offs like high co-pay ratios, sub-limits on treatments, or poor customer service reviews. Always compare the features first, and use the premium as a tie-breaker only when the features are identical.

Does my health policy cover diagnostic tests like MRIs and blood tests?

Usually, diagnostic tests are covered under pre-hospitalization and post-hospitalization expenses (typically 30 to 60 days before admission and 90 to 180 days after discharge), provided they are directly related to the illness that required hospitalization. Outpatient (OPD) diagnostic tests without hospitalization are only covered if you have a specific OPD cover rider.

How does cashless treatment actually work in an emergency?

In an emergency, you show your health card at the hospital’s TPA (Third Party Administrator) desk. They send an authorization request to your insurer. Once the insurer reviews the case, they issue an initial approval, allowing the hospital to begin cashless treatment. The final bill is settled directly between the hospital and the insurance company, minus any non-medical items.

The Final Word | Don’t Wait for the Storm to Build Your Roof

Here’s my parting thought. We often wait for a warning sign a minor health scare, a friend’s hospitalization, or turning a certain age before we start thinking about health insurance. But the brutal reality of life is that the best time to buy health insurance is when you don’t need it. Because when you do need it, no company will sell it to you.

Take an hour this weekend. Look at your current coverage, weigh it against the real-world costs of healthcare today, and make the adjustment. It is one of the few decisions in life where you will never regret spending a little extra for absolute peace of mind.