We have all been there. You open your banking app on a lazy Sunday afternoon, and there it is, flashing in bright green: “Congratulations! You are eligible for a pre-approved personal loan of ₹5,00,000.” It feels like an unexpected gift, a gentle nudge telling you that your dream vacation, that sleek new OLED TV, or even a fancy destination wedding is just a single tap away. But let’s be honest nothing in the financial world is truly free.

In today’s fast-paced economy, understanding How Personal Loans Work and When to Use Them is no longer just a piece of niche financial advice; it is a critical survival skill. Personal loans can either be a magnificent launchpad that helps you tide over a genuine crisis or a slippery slope that drags you into a suffocating cycle of debt. To make sure you stay on the right side of that equation, let’s pull back the curtain and look at how these financial instruments actually function beneath the shiny marketing brochures.

The Inner Mechanics | What Happens Behind the Bank Screens?

At its core, a personal loan is a form of unsecured personal loan . Unlike a home loan or a car loan, where the bank can seize your property if you default, an unsecured loan requires no collateral. The bank is essentially lending you money based on a promise your promise to pay them back with interest over a fixed period. Because there is no physical asset backing the loan, it falls under the category of unsecured debt , which naturally makes it riskier for lenders.

To compensate for this risk, banks examine your financial life under a microscope. This is where your financial track record comes into play. If you have a history of paying your bills on time, you are seen as a low-risk borrower. If not, you’ll find the door closed or, worse, you’ll be offered exorbitant rates. That’s why grasping How Personal Loans Work and When to Use Them can save you from making hasty commitments that harm your financial health.

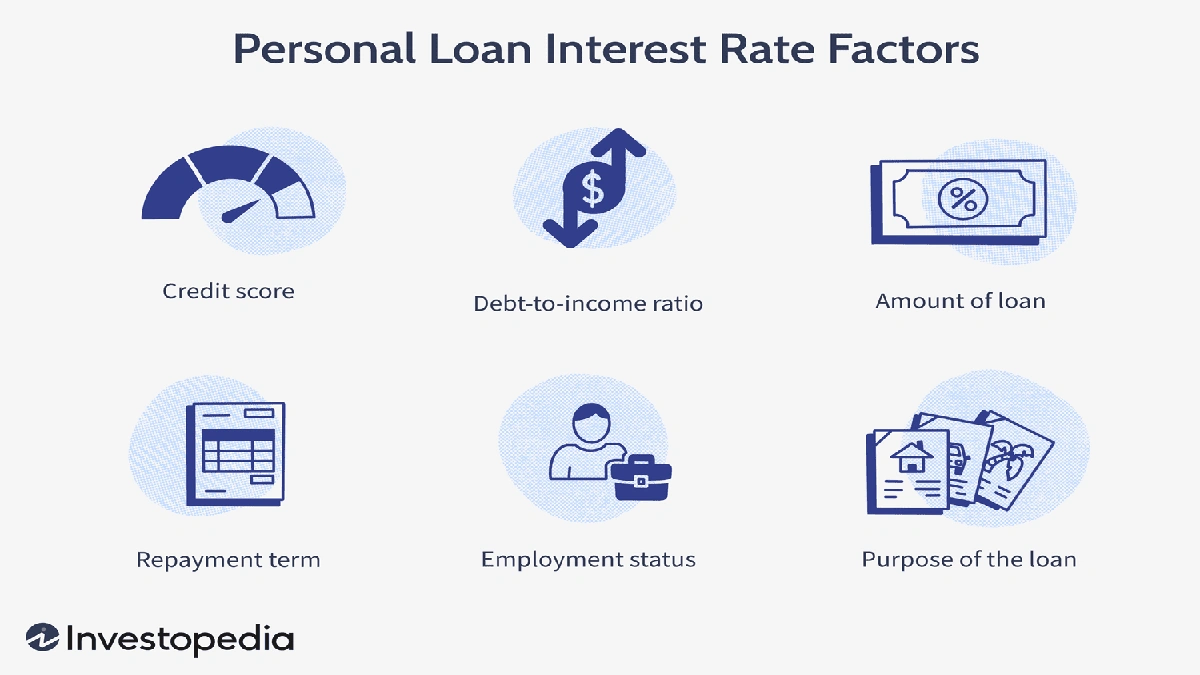

When you apply, the lender evaluates your application based on several key pillars:

- Your Income Stability: Lenders want to see a steady stream of income, whether you are salaried or self-employed.

- Debt-to-Income Ratio: If half of your salary is already going toward paying off other debts, lenders will hesitate to give you more.

- Credit History: This is your financial report card, summarizing your past borrowing and repayment habits.

Deciphering the Hidden Math of Borrowing

To truly master How Personal Loans Work and When to Use Them , we need to look past the monthly EMI number and understand the actual cost of borrowing. Many people fall into the trap of only looking at whether they can afford the monthly payment, completely ignoring how much extra money they will end up paying back in the long run.

First, let’s talk about interest rate options . Lenders generally offer two types of interest rates: flat rates and reducing balance rates. A flat interest rate calculates interest on the entire principal amount throughout the tenure, regardless of how much you have already paid back. On the other hand, a reducing balance rate calculates interest only on the outstanding loan balance. Always ask for the reducing balance rate; it is almost always cheaper.

Second, pay close attention to the loan repayment terms . While a longer tenure (like 5 or 7 years) reduces your monthly EMI, it drastically increases the total interest you pay. Conversely, a shorter tenure increases your monthly EMI but saves you a massive amount of money in interest. Let’s look at a quick comparison:

| Loan Amount (INR) | Interest Rate (p.a.) | Tenure (Years) | Monthly EMI (INR) | Total Interest Paid (INR) |

|---|---|---|---|---|

| ₹5,00,000 | 12% | 3 Years | ₹16,607 | ₹97,852 |

| ₹5,00,000 | 12% | 5 Years | ₹11,122 | ₹1,67,333 |

As you can see, extending the tenure by just two years costs you nearly ₹70,000 more in pure interest! This is why analyzing the term length is vital when figuring out the best borrowing strategy.

Smart Playbook | When Should You Actually Use a Personal Loan?

Now that we know how they work, let’s address the million-dollar question: when is it actually smart to take one? Here is a simple rule of thumb: use a personal loan only when it either saves you money, generates future value, or resolves an absolute emergency. Let’s break down the most sensible scenarios.

1. High-Interest Debt Consolidation

If you are juggling multiple credit cards with outstanding balances, you are likely paying interest rates as high as 36% to 42% per annum. Using an unsecured personal loan with an interest rate of 11% to 15% to pay off those cards is an excellent debt consolidation strategy . You replace multiple high-interest debts with a single, lower-interest monthly payment. This is a classic scenario where knowing How Personal Loans Work and When to Use Them prevents a minor crisis from turning into an absolute disaster.

2. Unavoidable Medical Emergencies

Life has a habit of throwing curveballs when we least expect them. If a family member requires urgent medical treatment and your health insurance policy doesn’t cover the entire bill, a personal loan can be a lifesaver. It gives you instant access to funds without requiring you to liquidate long-term investments like your PPF or mutual funds, which are meant for your retirement.

3. Investing in Career Transition and Upskilling

Sometimes, the best investment you can make is in yourself. If taking a specialized certification or a coding bootcamp can double your salary, but you don’t have the cash upfront, borrowing to finance this education can be highly justified. However, before doing this, ensure you have a clear plan. If you want to explore professional paths that don’t require heavy upfront costs, you might want to look into the best remote jobs for beginners 2026 to boost your monthly cash flow organically before taking on debt.

The Dangerous Traps to Avoid

Just as there are good reasons to take a loan, there are incredibly bad ones. Taking out debt for temporary lifestyle pleasures is a quick way to derail your financial future. Let’s call out these traps for what they are.

First, never take a loan to fund a luxury vacation, a lavish wedding, or the latest smartphone. These are depreciating assets or fleeting experiences. Paying off a vacation for three years after the tan has faded is a recipe for deep financial regret. If you are working on your overall financial plan, learning how to budget and manage your basic expenses is far more valuable than relying on quick credit. You can find excellent resources on structured financial planning over at Best Car Insurance Plan to help keep your budget balanced.Second, ignore credit score requirements at your own peril. Your CIBIL score is the first thing a lender checks. If you apply for loans with a low credit score, you will either face immediate rejection (which further damages your score) or be offered terrible personal loan interest rates that make borrowing incredibly expensive. Always aim to keep your credit score above 750 before even thinking about applying.

Once you grasp How Personal Loans Work and When to Use Them , you can spot these traps from a mile away and avoid the marketing gimmicks designed to make borrowing look effortless.

How to Secure the Best Deal Possible

Before you sign on the dotted line, remember that everything is negotiable. Do not simply accept the first pre-approved offer that pops up on your phone. Here is your checklist to get the best deal:

- Compare Lenders: Check rates across public sector banks, private banks, and reputed non-banking financial companies (NBFCs). Public sector banks often have slightly slower processing times but offer much lower interest rates.

- Negotiate Fees: Always ask the loan officer to waive or reduce the processing fee. Often, they have the authority to discount this fee to close the deal.

- Read the Foreclosure Terms: If you get a sudden bonus or windfall, you will want to pay off your loan early. Make sure your loan doesn’t carry heavy pre-payment penalty charges.

Before we wrap up this masterclass on How Personal Loans Work and When to Use Them , let’s look at a few common questions that many borrowers ask when navigating this landscape.

Frequently Asked Questions About Personal Loans

Can I pay off my personal loan before the tenure ends?

Yes, most banks allow prepayment or foreclosure. However, many private lenders charge a foreclosure fee ranging from 2% to 5% of the outstanding principal amount. Always read the fine print regarding prepayment penalties before signing the agreement.

How does applying for a personal loan affect my CIBIL score?

When you apply, the lender makes a hard inquiry on your credit report to assess your eligibility. While a single hard inquiry might dip your score by a few points temporarily, making multiple loan applications within a short window can make you look credit-hungry and significantly lower your credit score.

What is the minimum credit score required for a personal loan?

While some lenders might approve loans for lower scores at higher interest rates, a credit score of 750 or above is generally considered ideal. Maintaining a score in this range ensures you qualify for the most competitive interest rates and smooth processing.

Are there any tax benefits on personal loans in India?

Generally, personal loans do not offer tax benefits. However, there is an exception: if you can prove that the loan amount was used strictly for home renovation or to fund higher education, you may claim tax deductions under specific sections of the Income Tax Act.

Ultimately, mastering How Personal Loans Work and When to Use Them puts you in the driver’s seat of your financial future. Use credit as a precision tool, not a financial crutch, and you will find yourself building real, lasting wealth over time.